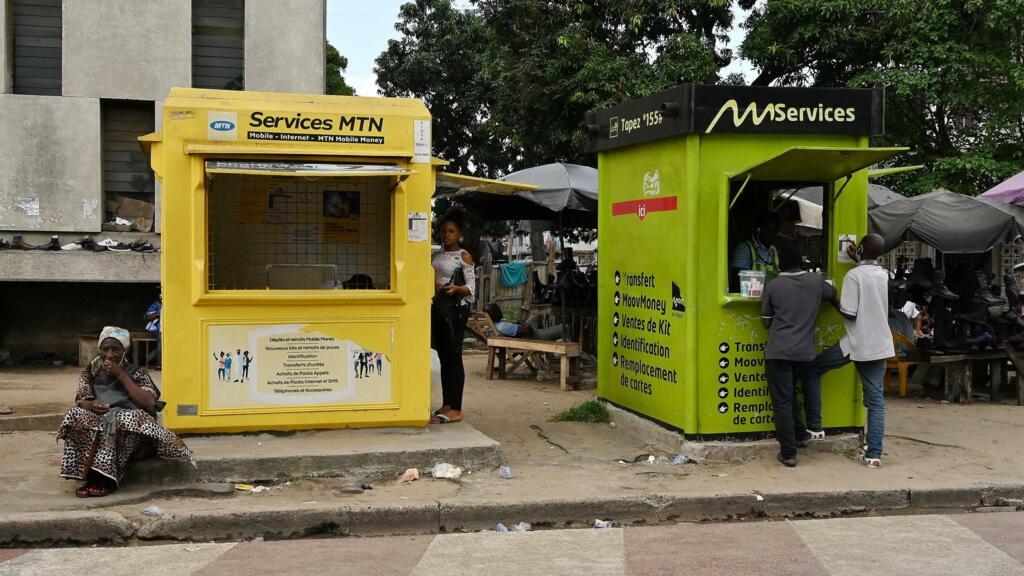

In the bustling streets of Côte d’Ivoire, mobile money kiosks have become more ubiquitous than traditional banks. With over 400,000 service points across the nation, these small booths outnumber automated teller machines by a staggering 300 to one. However, this massive network, essential for daily financial transactions, is currently grappling with a significant hurdle: a persistent shortage of physical cash.

As evening approaches in Abidjan’s Angré Château district, the rush for transportation and groceries begins. At a busy intersection, a mobile money kiosk stands unable to serve its clients. Rosette, a local resident hoping to withdraw 10,000 CFA francs (roughly 15 euros), expresses a sense of resignation. She notes that it is common to find agents who simply do not have the funds required, forcing customers to adapt to these frequent disruptions.

Inside the small yellow booth, Nema, the teller, manages a growing queue of disappointed patrons. She explains that high withdrawal volumes often deplete their reserves, leaving them with no choice but to apologize and inform customers that they can only accept deposits until they restock.

For shop managers like Affoué, a former accountant, every turned-away customer represents a direct financial loss. She emphasizes that losing a client means losing the associated commission, which is vital for covering overheads and generating a net profit. Maintaining a steady flow of transactions is the only way to keep the business viable.

The economics of commissions and downtime

In this ecosystem, major operators such as MTN, Orange, Wave, and Moov pay agents a small fee for each transaction. For a 10,000 CFA franc withdrawal, an agent typically earns between 20 and 60 CFA francs (roughly 3 to 9 euro cents). Success depends entirely on high volume and high-value transfers.

When cash or digital credit runs out, the business effectively stops. Agents are frequently forced to lock their doors and travel to banks or larger distributors to replenish their supplies. This downtime leads to a cycle of lost revenue and declining customer loyalty, as the service becomes unreliable.

Innovative solutions on two wheels

To address this bottleneck, Gertrude Yapi, the operations director at the startup Leya, has launched a specialized courier service. Using a fleet of motorcycles, Leya delivers digital credit and physical cash directly to kiosks across the city. Digital top-ups take less than four minutes, while cash deliveries are completed within half an hour.

This rapid response allows vendors to increase their turnover by up to 50%. Currently, Leya serves over 3,000 active clients across four major Ivorian cities: Abidjan, Bouaké, Korhogo, and Bondoukou.

Economist Kassoum Timité highlights the broader implications of these liquidity issues. He points out that mobile money is the lifeblood of the informal sector, which accounts for nearly 40% of the Ivorian GDP. Any slowdown in these micro-transactions inevitably ripples through the entire national economy.

The scale of the industry is immense. By 2024, daily transactions reached over 140 billion CFA francs (approximately 210 million euros), a fourfold increase compared to the figures recorded in 2020. As the sector continues to expand, solving the liquidity crisis remains a top priority for economic stability.