UEMOA’s Financial System Under Strain as Niger’s Default Rate Soars

The latest economic outlook report for January 2026 exposes stark vulnerabilities within the West African Economic and Monetary Union (UEMOA). While the regional banking sector achieves symbolic milestones, a surge in non-performing loans threatens its stability. At the epicenter of this crisis stands Niger, whose staggering default rate has widened the economic divide within the union.

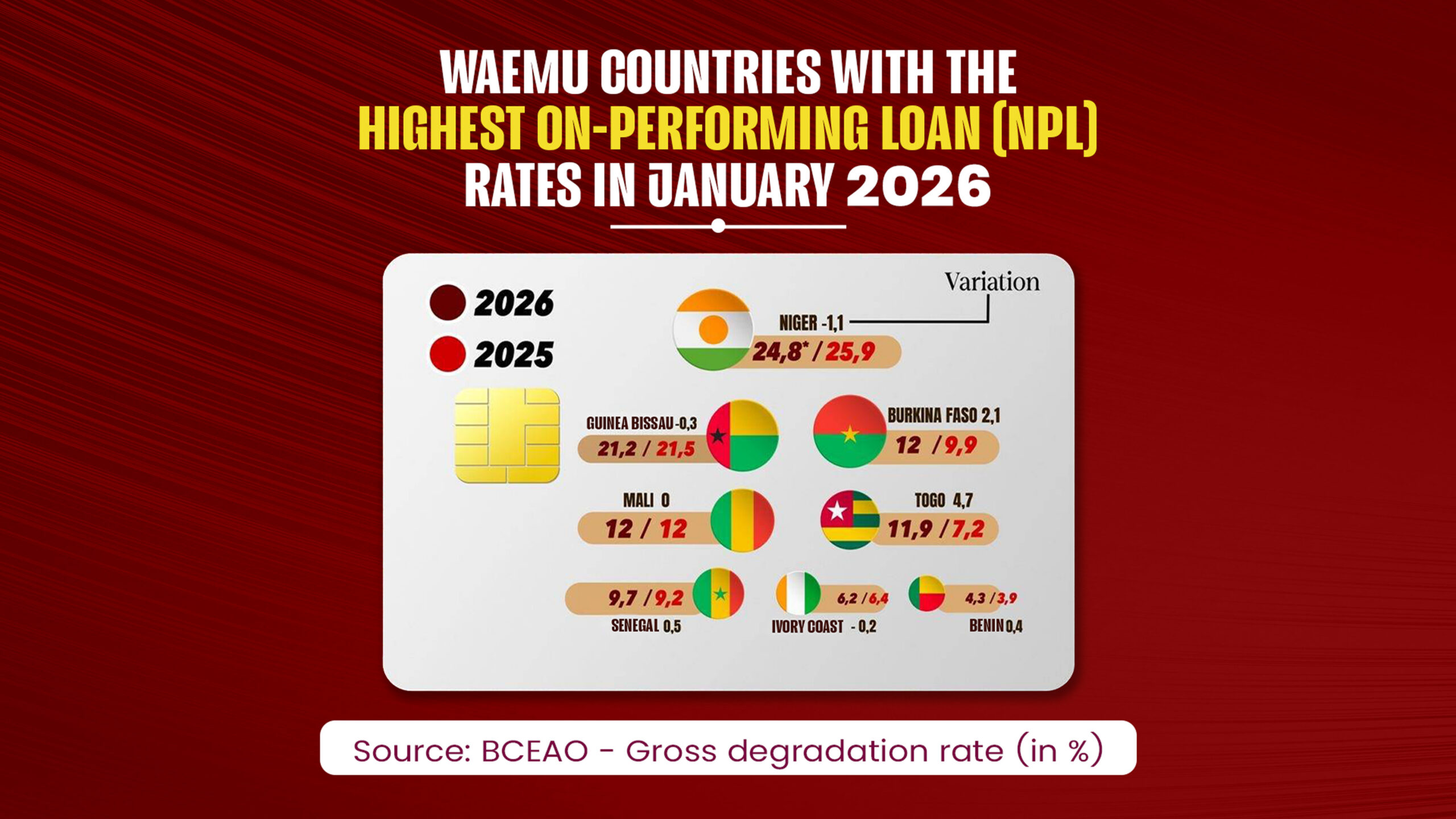

Niger’s Alarming Financial Vulnerability

Despite marginal improvements, Niger remains the most fragile link in the UEMOA banking chain. The country’s non-performing loan (NPL) ratio stands at a precarious 24.8%—far exceeding regional norms and signaling deep-rooted structural weaknesses.

Though the rate has dipped slightly from 25.9% in 2025, the disparity between Niger and its peers underscores an alarming exposure to systemic risk. Persistent security challenges and political instability continue to erode investor confidence, exacerbating the financial strain.

A Divided Union: Coastal Stability vs. Sahelian Crisis

The January 2026 data highlights a widening rift between UEMOA’s coastal economies and its Sahelian bloc, where Niger serves as the crisis’s focal point.

The Sahelian Bloc’s Precarious Position

The region’s financial fragility is most acute in the following countries:

- Mali and Burkina Faso: Both nations register NPL rates of 12%, with Burkina Faso experiencing a sharp year-on-year increase of 2.1 percentage points.

- Guinea-Bissau: Despite a slight improvement, its NPL ratio remains critically high at 21.2%.

The Coastal Bloc’s Relative Resilience

Contrasting with the Sahel, UEMOA’s coastal economies demonstrate greater financial stability, though not without concerns:

- Benin: Leads the union with the lowest NPL rate of 4.3%, setting a benchmark for fiscal discipline.

- Ivory Coast and Senegal: Maintain moderate stability, with rates of 6.2% and 9.7%, respectively.

- Togo’s Outlier Surge: The country defies regional trends with a dramatic spike in defaults, jumping from 7.2% to 11.9% (+4.7 points).

Loan Portfolio Expands, but Risks Mount

The UEMOA’s total loan portfolio has surpassed 40,031 billion FCFA—a historic high, marking a 4.7% annual increase. Yet this growth is overshadowed by escalating risks.

Non-performing loans now total 3,631 billion FCFA, pushing the coverage ratio to a concerning 59%. This figure reveals a troubling lag in banks’ ability to absorb losses as defaults accelerate.

Banks Tighten the Reins on Lending

In response to the deteriorating risk landscape, particularly in Niger, financial institutions are adopting defensive strategies:

- Stricter Lending Criteria: Higher personal contributions and collateral requirements deter borrowers.

- Selective Expansion: Banks prioritize balance sheet safety over credit growth, potentially stifling funding for local SMEs and MSMEs.

As the UEMOA navigates this pivotal moment, the systemic vulnerabilities exposed by Niger’s crisis demand heightened scrutiny. While the union’s financial foundations remain intact, the looming threat of a liquidity crunch necessitates immediate and coordinated action to prevent broader contagion.